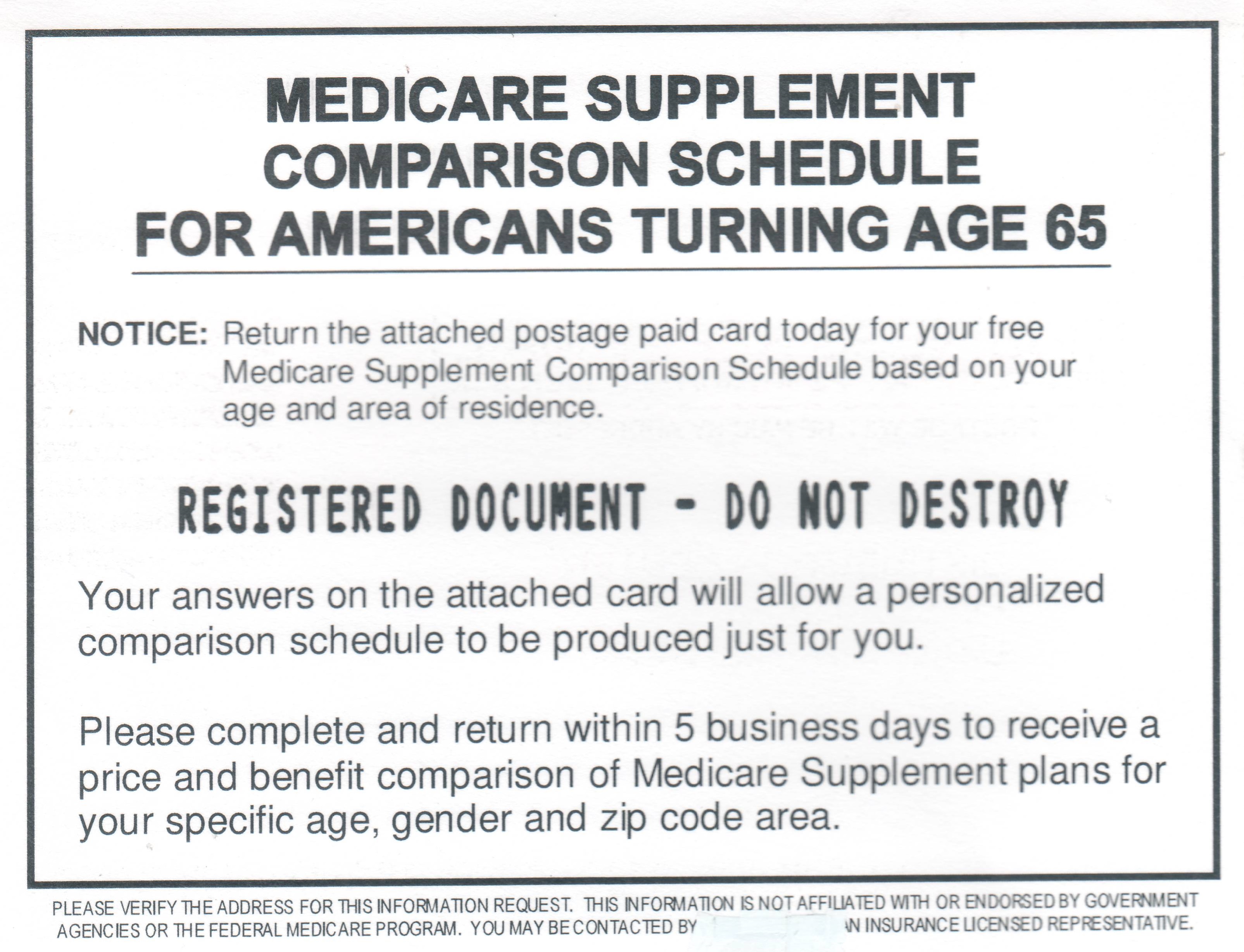

Have you received this postcard in the mail? Is it coming from Medicare? Is it important information? It does say, “REGISTERED DOCUMENT – DO NOT DESTROY.” The truth is this is just a solicitation for insurance, and if you mail in the return postcard you are sure to get a call from an insurance agent, or worse yet a knock on your front door. The unfortunate truth is we now live in a world of information overload and everyone is vying for your attention…yes, even me. And in the world of Medicare, some lead companies resort to making the older population believe their mailing is more than it is.

Have you received this postcard in the mail? Is it coming from Medicare? Is it important information? It does say, “REGISTERED DOCUMENT – DO NOT DESTROY.” The truth is this is just a solicitation for insurance, and if you mail in the return postcard you are sure to get a call from an insurance agent, or worse yet a knock on your front door. The unfortunate truth is we now live in a world of information overload and everyone is vying for your attention…yes, even me. And in the world of Medicare, some lead companies resort to making the older population believe their mailing is more than it is.

If you look closely at the small print at the bottom you will read, “This information is not affiliated or endorsed by government agencies or the federal Medicare program. You may be contacted by an insurance licensed representative.” This disclaimer language is a sure sign that the mailing is a solicitation as it is required by Medicare. I am not judging those who use these postcards to drum up business, in fact these cards are completely compliant with current regulations. I just believe there is a better way…honesty!

Why can’t we replace the words, “REGISTERED DOCUMENT – DO NOT DESTROY” with, “THIS IS NOT A REGISTERED DOCUMENT – DESTROY IF YOU WANT…BUT IF YOU DO, OUR AGENCY WON’T BE ABLE TO HELP YOU!” Why can’t we just get back to letting people know we are here to help when they need it.

Here is a great example:

https://www.youtube.com/watch?v=FrmYLo3tMA8